Interest Rate Caps: A Tool for Financial Exclusion?

When MSMEs are asked what they think of interest rates, it is not surprising that they find it too high. When asked whether they think that access to finance is difficult, it is not surprising that they find that it is. The problem with arriving at any conclusion based on these types of questions is that it is meaningless. Everyone would prefer that their loans carried lower interest rates and were easier to access.

The average lending interest rate of 107 countries for which data was available for 2018 on the World Development Indicators[1] was 11.40%. However, these included four countries with rates in excess of 30% where Madagascar is approaching 60% and Brazil and Argentina are approaching 40%. Another five countries have rates in excess of 20%.

We may ask what a reasonable interest rate is. However, any interest rate that is suggested as being reasonable is nothing but an arbitrary figure. In fact, reasonableness can only be judged relative to each country’s financial environment. The fact that loans with an interest rate of 60% are being serviced by businesses in Madagascar suggests it is sustainable, albeit loan portfolio growth prospects may appear to be limited.

In a project where I was working with a financial institution to develop an appropriate product for a specific MSME sector, a target group of very small businesses were asked if an 18% per annum interest rate would be appealing to them. Their response was positive because it would be a significant reduction from the 27% that they were paying to a microfinance institution. What is important to note is that these businesses had already demonstrated that they were able to service the higher interest loans. To the financial institutions this track record provided significant comfort. However, it is even more important to note that in the absence of an offer for the lower interest rates, the businesses would continue to borrow at the higher rate from the microfinance institutions.

It is not a big leap to say with complete certainty that they would be agreeable to 9%, if offered. However, in this case, the financial institution was not interested in lending to that sector below 18%. No financial institutions had ever offered such a low rate to these borrowers. It was a win for all concerned. Using the same logic, the prospect of receiving financing at 27% in Madagascar would no doubt be received in a similar way to the example mentioned above. Here also, it is not the interest rate being offered. Therefore, the question to ask is whether it is more important to have access to finance for more businesses or to have lower interest rate loans for a fewer businesses.

When MSMEs are asked what they think of interest rates, it is not surprising that they find it too high. When asked whether they think that access to finance is difficult, it is not surprising that they find that it is. The problem with arriving at any conclusion based on these types of questions is that it is meaningless. Everyone would prefer that their loans carried lower interest rates and were easier to access.

The average lending interest rate of 107 countries for which data was available for 2018 on the World Development Indicators[1] was 11.40%. However, these included four countries with rates in excess of 30% where Madagascar is approaching 60% and Brazil and Argentina are approaching 40%. Another five countries have rates in excess of 20%.

We may ask what a reasonable interest rate is. However, any interest rate that is suggested as being reasonable is nothing but an arbitrary figure. In fact, reasonableness can only be judged relative to each country’s financial environment. The fact that loans with an interest rate of 60% are being serviced by businesses in Madagascar suggests it is sustainable, albeit loan portfolio growth prospects may appear to be limited.

In a project where I was working with a financial institution to develop an appropriate product for a specific MSME sector, a target group of very small businesses were asked if an 18% per annum interest rate would be appealing to them. Their response was positive because it would be a significant reduction from the 27% that they were paying to a microfinance institution. What is important to note is that these businesses had already demonstrated that they were able to service the higher interest loans. To the financial institutions this track record provided significant comfort. However, it is even more important to note that in the absence of an offer for the lower interest rates, the businesses would continue to borrow at the higher rate from the microfinance institutions.

It is not a big leap to say with complete certainty that they would be agreeable to 9%, if offered. However, in this case, the financial institution was not interested in lending to that sector below 18%. No financial institutions had ever offered such a low rate to these borrowers. It was a win for all concerned. Using the same logic, the prospect of receiving financing at 27% in Madagascar would no doubt be received in a similar way to the example mentioned above. Here also, it is not the interest rate being offered. Therefore, the question to ask is whether it is more important to have access to finance for more businesses or to have lower interest rate loans for a fewer businesses.

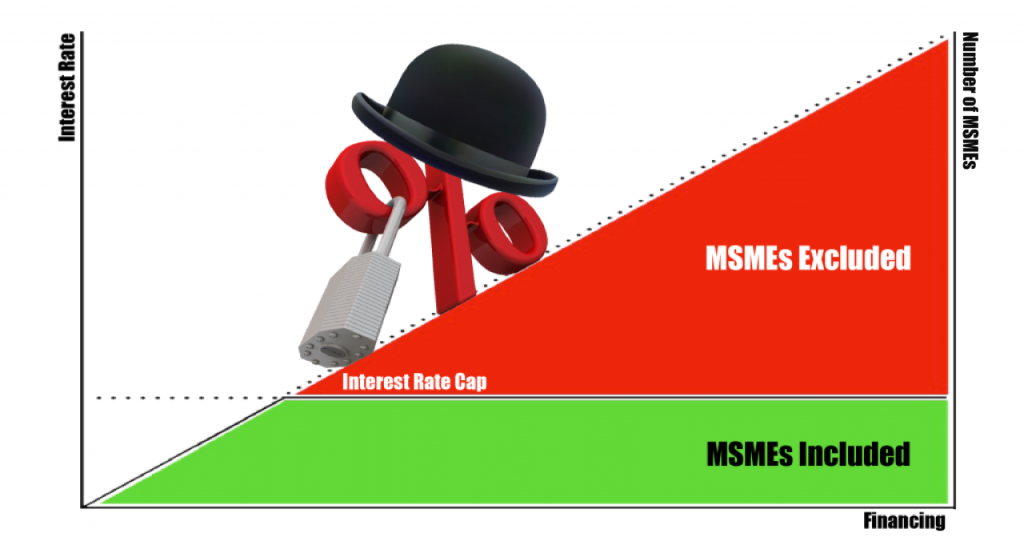

Numerous studies[2] have shown that attempting to reduce interest rate through caps in an effort to make loans more affordable actually decrease access to finance. Intuitively this seems to make sense. A financial institution that has comfort and ability to lend to large businesses will only enter the small and medium enterprise space if they are able to earn significantly higher spreads. What that spread is, depends entirely on the demand and supply of credit to that segment of the economy.

Although some governments have combined interest rate caps with mandatory minimum lending requirements in favor of underserved segments for financial institutions, these measures often end up excluding the very people the cap was trying to help. When forced to lend to a sector that financial institutions have little comfort or interest in, the volume of loans generally never exceed the minimum requirements. For the most part these are considered a cost of doing business rather than an opportunity to open up a new business segment. In fact loss minimization often becomes the key focus. This means that the financial institutions end up financing only those MSMEs that they would have lent to anyway and qualify under the criteria set by the government mandate. No additional effort is exerted in increasing the number of loans in excess of the minimum requirement because the spreads are not big enough for the perceived risks that the financial institution is taking. As a result, the main target beneficiaries of the mandate are often excluded.

Therefore, the best way to ensure that there is increased supply of finance to the financial excluded is to allow the financial institutions the freedom to charge the interest rates that the market will bear. Again, interest rate on loans to MSMEs need to be market driven to generate sufficient interest by the financial institutions. These rates can only be sustainably reduced in the long term through growth in competition among financial institutions to lend to MSMEs.

More financial institutions will start entering the MSMEs space, initially because of the significantly higher spreads compared to loans to large businesses. Later they will target the MSME segment because the financial institutions will have realized that MSMEs are viable businesses that offer better returns on investment as a portfolio than large business loans. The creation of a situation where the supply of finance is greater than the demand will force the interest rates on MSME loans down to more ‘reasonable’ levels. It not a short term play.

[1] World Development Indicators: https://databank.worldbank.org/reports.aspx?source=2&series=FR.INR.LEND&country=# (Last Updated December 20, 2019)

[2] Helms and Reille 2004; Porteous, Collins, and Abrams (2010); Laeven (2003); and Munzele and Henriquez Gallegos (2014).