The Collateral Stranglehold: Why Access the Finance Elude MSMEs

After nearly three decades in finance, I’ve seen too many viable businesses fail simply because they couldn’t pledge a building as security. The paradox of MSME finance continues to frustrate me after 30 years in this field. We have more financial tools than ever before to reduce dependence on traditional collateral, land and buildings, the usual suspects that have locked out millions of viable businesses from credit. Yet across the 16 countries where I’ve worked, the story remains depressingly similar: “Show us your title deed, or show yourself the door.”

This collateral obsession is more than just conservative banking. It’s a systemic failure that perpetuates inequality and stifles economic growth precisely where it’s needed most. The irony is that there exist ready built solutions. They’re sitting there, underutilized, while MSMEs continue to suffocate from lack of access to finance.

Microfinance institutions understood this challenge decades ago and built entire business models around alternatives to traditional collateral. But they’ve largely remained in their own ecosystem, serving the smallest enterprises while the broader MSME sector struggles to find similar innovation from mainstream banks.

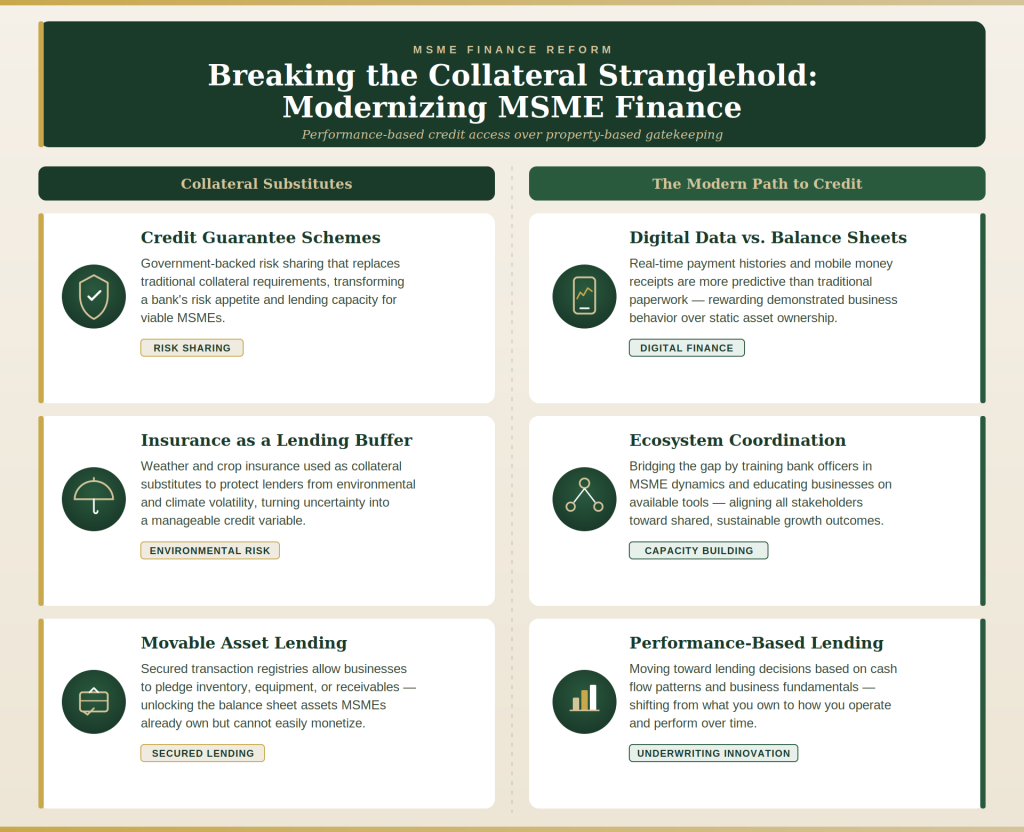

Credit guarantee schemes, which I’ve designed across six regions, exist precisely to replace collateral requirements with government-backed risk sharing. When properly structured, they can transform a bank’s risk appetite overnight. Yet too many schemes remain underutilized because neither MSMEs nor banks truly understand how to leverage them effectively.

Insurance products, particularly weather and crop insurance in agricultural lending, can serve as excellent collateral substitutes. A farmer with comprehensive crop insurance presents a fundamentally different risk profile than one exposed to weather volatility. Financial institutions can lend against these risk mitigation tools rather than demanding land titles that many smallholder farmers simply don’t possess.

Leasing and factoring products should be standard offerings in any mature financial market, allowing businesses to access equipment financing or working capital without traditional collateral. Yet in many developing markets, these products remain scarce or nonexistent among mainstream financial institutions.

Perhaps most exciting are the opportunities that fintech presents for revolutionizing how we assess MSME creditworthiness. When a business processes payments digitally, it creates a transaction history that tells a far more accurate story than any balance sheet. Cash flow patterns, customer diversity, seasonal variations — all visible in real-time payment data.

This isn’t theoretical. Digital transaction histories are already proving more predictive of repayment behavior than traditional financial statements in many contexts. A small retailer with consistent daily card transactions and mobile money receipts presents a clearer risk profile than one with pristine paperwork but no transaction visibility.

Secured transactions registries (collateral registries) offer another underexploited tool, allowing businesses to pledge as security non-traditional collateral, namely, movable assets (inventory, equipment, receivables, etc.). Combined with credit information bureaus that provide historical performance data, these systems can support lending decisions based on business reality rather than property ownership.

The fundamental problem isn’t lack of tools. It’s lack of coordination. We have guarantee schemes that MSMEs don’t know about, fintech solutions that banks don’t trust, insurance products that aren’t integrated into lending decisions, and blended finance facilities that remain underutilized because of information gaps.

Blended finance products, typically offered through partnerships between development finance institutions and commercial banks, can dramatically improve MSME access to credit. But these partnerships often fail to reach their target beneficiaries because MSMEs lack information about available products while participating banks lack deep understanding of MSME operations and needs.

This coordination failure represents a massive opportunity cost. Every viable MSME that remains unfunded because of collateral constraints is a missed opportunity for job creation, innovation, and economic growth. The businesses I’ve encountered over the years that could have thrived with proper financing access represent billions in foregone economic activity.

What we need is a cohesive strategy that bridges the information gap from both sides. MSMEs need comprehensive education about alternative financing options. This is not just about product awareness, but practical guidance on how to prepare for and access these facilities. Many businesses that could qualify for guarantee scheme support or fintech-enabled lending simply don’t know these options exist.

Simultaneously, financial institutions need deeper training in MSME sector dynamics. Understanding seasonal cash flows in agriculture, working capital cycles in manufacturing, or customer payment patterns in services requires sector-specific knowledge that many loan officers lack. Managing MSME lending risks effectively requires different skills than corporate lending.

The path forward requires orchestrated effort from governments, development partners, and financial institutions. We must move beyond creating individual products toward building integrated ecosystems where MSMEs can access appropriate financing based on their business fundamentals rather than their property holdings.

After three decades of watching this slow-motion crisis unfold, I’m convinced we have the tools to solve it. What we lack is the coordination and commitment to deploy them systematically. The cost of continued inaction — measured in jobs not created, innovations not funded, and communities not developed — demands urgent attention. The collateral stranglehold on MSME finance can be broken. We just need to decide we’re serious about breaking it.